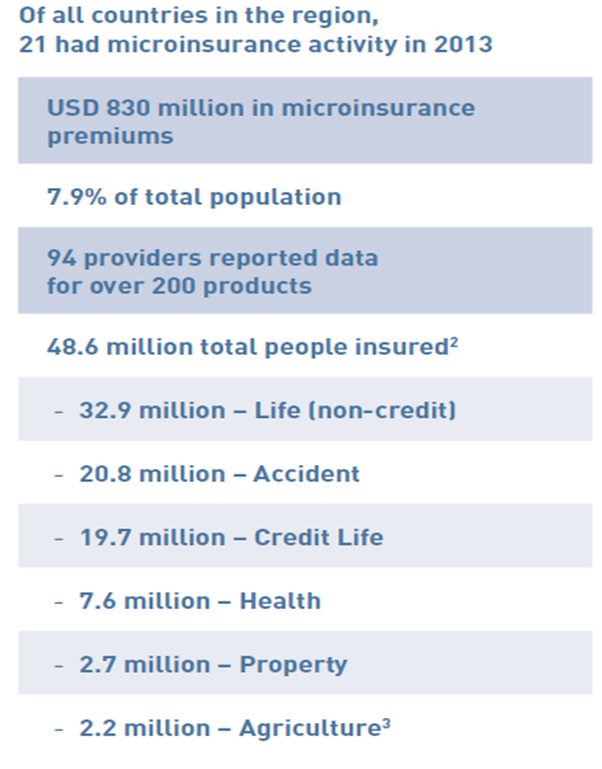

The full report is not out yet, however we get a glimpse at the data via a preliminary briefing note due in Q1 2015. The study identified 48,6 million people covered in Latinamerica and the Caribbean (45,5 million had been identified in 2012 on 2011 data), i.e., 6,8% more lives covered than in 2011. The “microinsurance explosion” observed between 2005 and 2011 (14% CAGRs) has shifted towards a slower growth phase with continued dominance of life and accident products.

The full report is not out yet, however we get a glimpse at the data via a preliminary briefing note due in Q1 2015. The study identified 48,6 million people covered in Latinamerica and the Caribbean (45,5 million had been identified in 2012 on 2011 data), i.e., 6,8% more lives covered than in 2011. The “microinsurance explosion” observed between 2005 and 2011 (14% CAGRs) has shifted towards a slower growth phase with continued dominance of life and accident products.

Eight institutions have entered the market in recent years and many others have launched new products, yet there has been very limited evolution in terms of the types of products offered. New products launched since 2011 still largely cover life or personal accident, with very few lives being reached with health, property, or agriculture covers.

Key findings included:

Towards mass market insurance. A significant number of products were discontinued or altered to appeal to the mass market. However, due to limited growth in outreach by products that continued across the study period 2011 to 2013, this has resulted in slow growth in terms of total lives insured in the region, and limited evolution in terms of product diversity. This situation may in part reflect the overall trend towards mass market insurance in the region. The lack of product diversity may be the consequence of the increasing availability of social security programmes throughout the region, which may reduce the perceived opportunities to offer certain microinsurance policy types, e.g. health.

Increasingly diverse distribution channels. There still exist a wide variety of distribution channels. Though MFIs remain a key distribution channel, other non-traditional channels such as retailers, utilities, mobile network operators (MNOs), and banking correspondents, reach on average more people per product and in addition offer a surprisingly high proportion of the primary health and property covers in the region. Even though these new alternative channels facilitate greater outreach, they often apply higher commissions, potentially decreasing value for clients. The complexity of products offered is also more limited.

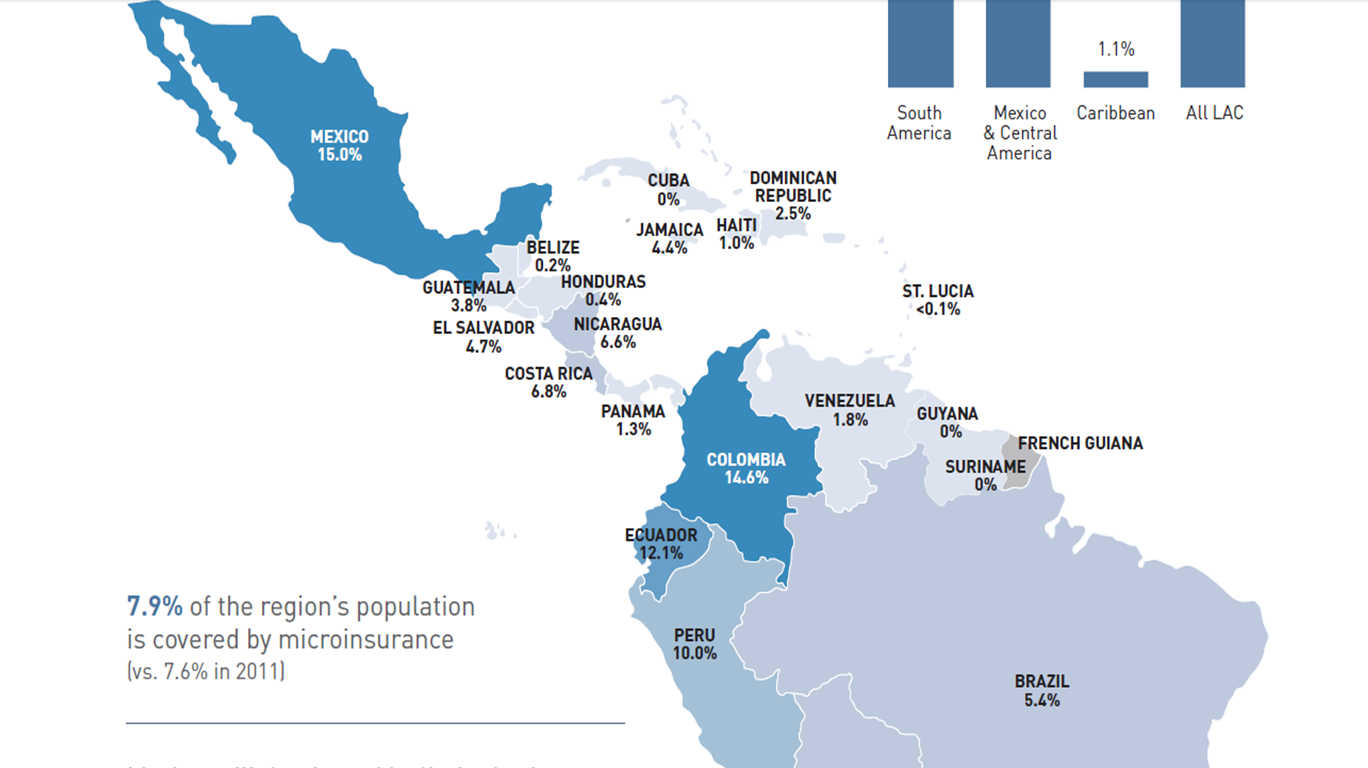

Slow increase in covered lives. Compared to 2011 when 7,6% of the population was identified as “covered”, the 2013 data suggests a total coverage of 7,9%.

Slow increase in covered lives. Compared to 2011 when 7,6% of the population was identified as “covered”, the 2013 data suggests a total coverage of 7,9%.

Only little product diversification. The market is still dominated by limited value

life and accident products, comprising 85% of all identified covers (vs. 84% in 2011).

A few key performance indicators.

- Premiums: USD 830 million

- Median commission rate: 20% (21% weighted average)

- Median loss ratio: 25% (26% weighted average)

ok, these are some initial results on LAC. Once the “real” study is out, you will definitely get an update on this blog.

In this series of microinsurance blogs, please also find:

Microinsurance 101

Microinsurance in Africa

Microinsurance in Asia