Study by BFA and MicroSave, commissioned by CGAP

It sounds obvious that people using digital financial services (DFS) will stop using the services if their confirmation sms does not arrive, if they do not know if their money has been transferred or their utility bill has been paid.

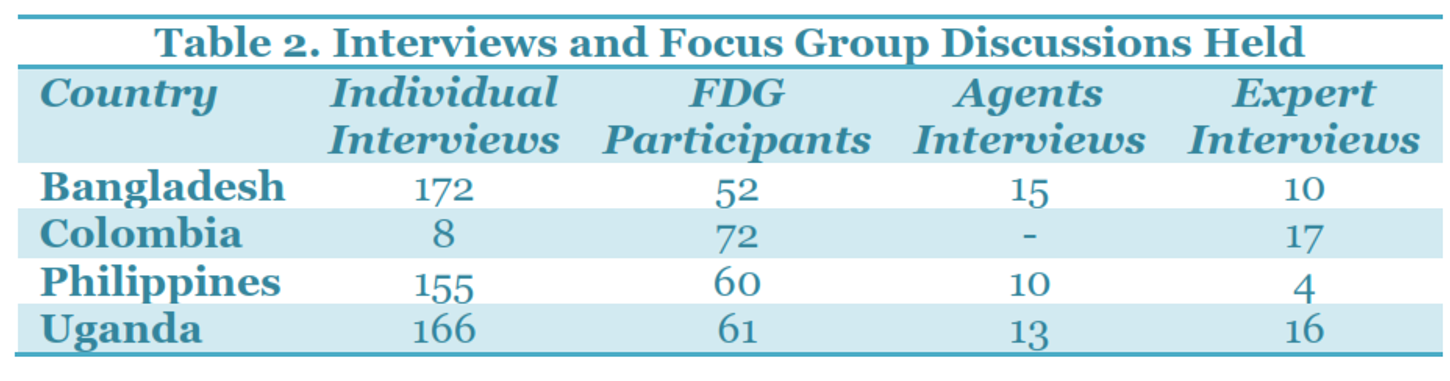

CGAP has now commissioned MicroSave and BFA to examine the risks that consumers are exposed to with DFS which can significantly reduce the profitability of the service, affect users trust and perception, but also uptake and usage. The research was done in four countries (Bangladesh, Colombia, Philippines, and Uganda) primarily for their maturity and different market profiles. Sample sizes were fairly small since the studies were not supposed to be nationally representative.

Methodology

Overall, the findings let conclude that DFS are needed and appreciated by users. The value proposition is even so strong that many customers overlook or tolerate challenges they encounter with the service. In Bangladesh, Philippines and Uganda,the service is a simple personal remittance offer (P2P) where as in Colombia it is more geared towards utility payments (P2B). However, challenges in the customer service affect the customer experience, reduce trust, uptake and usage. The study identified 3 common main issues:

Service downtime is the biggest issue in all four countries studied. The reasons are often very diverse including interconnection challenges between systems of banks and MNOs, limited bandwidth to mobile money, and limits on the USSD session time allowed for customers to complete transactions. In Uganda, MNO’s mobile money systems are struggeling to keep up with market growth.

Service downtown causes inconvenience, erodes trust, and can be very frustrating for customers. Without easy Access to money, people miss important opportunities, deadlines to pay certain things. Some clients will leave their money with the agent to terminate the transaction once the service is back up – creating a significant risk of fraud. For example, in Colombia, the “jineteo” service is growing by which clients deposit cash with agents to pay their bills. The agent will use the funds for personal purposes and pay the bills last minute.

Unauthorized fees/over-charging is common practice by agents not displaying approved Price lists for the Services they provide. Customers are left unsure of the cost of the service and often form the Impression that they are being overcharged. Unauthorized fees are most often charged for over-the-counter (OTC) transactions since These transactions already involve cash. In Uganda, customers started to believe that all fees charged by agents would be unauthorized and fraudulent.

Customers have less willingness to transact and the unauthorized charges create real cost for customers. Many will accept the higher fee since OTC transactions reduce the risk of sending Money to a wrong number. They see it more as a premium paid to protect themselves from the high cost of sending it to a wrong number. However this is definitely not the Long-term solution, not for customers, nor for providers.

Agent illiquidity is also common and results in the loss of customers’ access to their funds. In Uganda, customers are denied transactions or have to visit 2-3 other agents to send or receive their Money. In Bangladesh, cash management is a lot more sophisticated, this is less of an issue. In Colombia this issue was also not mentioned, probably because of their Focus on bill payments.

Agent illiquidity means no access to one’s funds, it results in split transactions which increases transaction fees and time for the Client, it reduces trust of users and potential users.

The issues below are more confined to specific countries in the study:

Country profiles

Sending Money to a wrong number and therefore losing it is a common challenge in Uganda and a strong fear in Bangladesh. This evidently is driving the popularity of OTC transactions.

Risks related to compromised PINs are often experienced in Uganda with its extensive history of DFS fraud. It is not sufficient to think about unscrupulous agents or friends/relatives, but there are also complicated procedures to unblock accounts when PINs are forgotten or after a customer makes three unsuccessful attempts to enter a PIN.

Lack of available agents is a Philippine-specific risk. As of December 2013, there were 24,000 registered agents with only 10,000 being active. Being an archipelago of more than 7,000 islands and with a huge population, is number is definitely too low.

But what are the consequences? Fear and perceptions reduce uptake and usage. Many customers become inactive since they are unable to transact or find it to scary. Others might use OTC transactions rather than keeping funds in their wallets.

Consequences might also involve deteriorating reputation of DFS and their providers, as well as less profitability of the mobile money services. With only 34.4% of registered users transacting, active user registration is effectively three times as expensive.

Do we maybe have to think about social performance (client protection) standards for mobile money providers?