CGAP recently launched a CGAP brief “Driving Scale and Density of Agent Networks in Perú” based on a CGAP-led research on 26,000 banking agents and 24 million monthly transactions to describe the relationship among factors that will help these agent networks to operate viably in more remote areas of the country.

CGAP recently launched a CGAP brief “Driving Scale and Density of Agent Networks in Perú” based on a CGAP-led research on 26,000 banking agents and 24 million monthly transactions to describe the relationship among factors that will help these agent networks to operate viably in more remote areas of the country.

Having spent so much time on the Latinamerican “correspondentes non bancarios” during my time with the CGAP Technology Team, I am excited to write again about what the agents have changed in terms of access to finance in many Latinamerican markets. Since 2005, banks in Peru are allowed to roll out agent networks.

There banks , like BCP, BBVA or Interbank, have been very active in rolling out their agent networks, compared to some of the microfinance institutions or cooperatives. In addition, to these often very large networks, third-party platforms, such as GloboKasNet, have emerged to link various banks, MFIs and cajas to a common payment platform, meaning that one KasNet agent may offer services on behalf of multiple financial institutions.

With today more than 24,000 agents, CGAP had launched a blog post “An Analysis of Peru´s cajeros corresponsales” in 2008 where the country was still showing only 2,400 agents ranking forth after Brazil, Philippines, and South Africa. A report from the Global Partnership for Financial Inclusion on Peru describes this impact on access to finance very impressively: Between June 2004 and June 2013:

- The number of service points in the financial system (branches, ATMs and banking agents) increased to almost 32,000, resulting in the service points per 100,000 adults increasing from 20 to 188.

- Usage indicators also indicate significant improvements in the use of financial services.

- The number of individuals holding a bank account increased from 9 million to 20 million during the same period.

- Percentage of districts with access to financial services rose to 43%, serving 87% of the total population.

- The data also revealed that banking agents have become the main channel used by financial institutions to expand their retail networks, especially in areas where opening a branch would be costly.

- By June 2013, the financial system had over 24,000 banking agents across the country.

- Percentage of adults with formal loan accounts has increased from 14% to 30%.

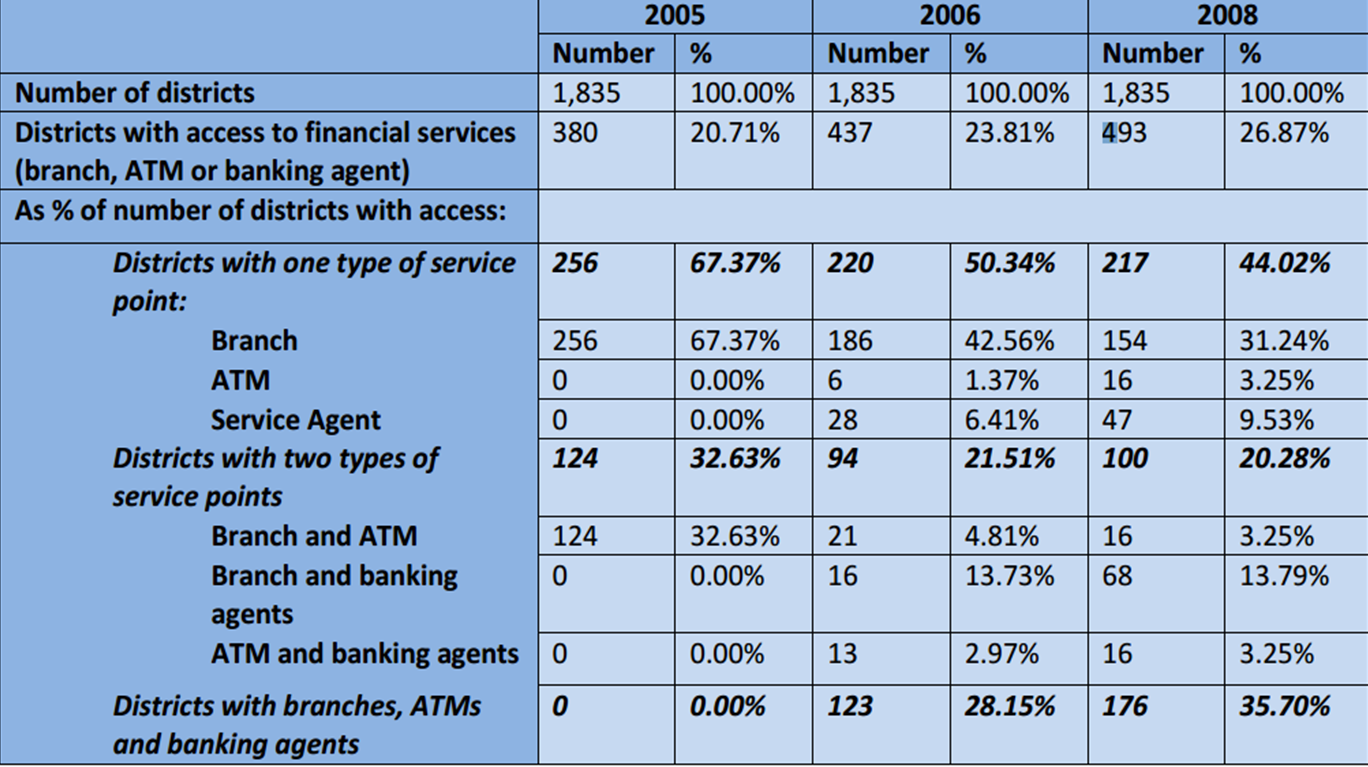

In the picture below, one can see the impact of the banking agent regulation in 2005 on access to finance:

However, there is still a large part of the population without access to financial services, especially in rural and low population density areas. To address this, regulation has been fine-tuned over time, with the aim the gap to be filled in financial inclusion is still wide, mainly in rural and low population density areas. Some of these “access” friendly regulation changes include:

However, there is still a large part of the population without access to financial services, especially in rural and low population density areas. To address this, regulation has been fine-tuned over time, with the aim the gap to be filled in financial inclusion is still wide, mainly in rural and low population density areas. Some of these “access” friendly regulation changes include:

Introducing a simplified account which can be immediately opened at the agent having him/her do the KYC (only asking for clients´ID) without asking the client to come to the branch. The simplified account are defined as low-value accounts subject to strict transaction and maximum balance limits; account balance cannot exceed the equivalent to $720 and monthly transactions cannot exceed $ 1,440. Uptake of these accounts were however slow and it is hoped that the development of mobile financial services will drive the use of these accounts. Since September 2013, banks have to report on the number of these accounts among their general account base,

Regulation of Emoney. Up to today, electronic money is prohibited in Peru and its regulation completely undefined. Branchless banking has taken the form of third-party agents, generally small business owners, offering cash-in cash-out services, and utility and (micro)loan payments. Rather than customers using mobile phones, agents transact through a POS device which communicates with the financial institution through a satellite chip or internet connection. There is a report by BBVA Research “The potential of mobile banking in Peru as a mechanism for financial inclusion” which spells out fairly clearly the challenges and opportunities around mobile money in Peru.

So the current e-money law from 2012 (29985) provides the following features:

- It is stored in electronic format

- It is accepted as a payment method by entities or individuals other than the issuer and is officially valid for payment

- It is issued for a value equal to the funds received

- It is convertible for cash as per the monetary value the holder has available. The contract shall clearly and expressly stipulate the cash reconversion terms and conditions, which shall be notified to the e-money holder.

- It is not a deposit nor does it earn interest. It is therefore not supported by the Deposit Guarantee Fund.

ok…. so I guess this is an exciting market to monitor going forward. Let me get back to you in 3 months (April 2014) to see where/if mobile money has taken off in Peru.