Wouldn´t it be great to better understand the financial lives of low-income clients? How they prefer to save, to whom they lend money to borrow from them at a later stage, how many times they experience a family emergency, etc. etc. etc. This kind of data was presented in August 2014 in the Kenya Financial Diaries.

Wouldn´t it be great to better understand the financial lives of low-income clients? How they prefer to save, to whom they lend money to borrow from them at a later stage, how many times they experience a family emergency, etc. etc. etc. This kind of data was presented in August 2014 in the Kenya Financial Diaries.

These in-depth results of having interviewed 300 low-income households every 2 weeks for a whole year in 5 different areas gives one the understanding of the financial lives of low-income Kenyans by capturing all of their transactions. The survey did not intend to capture a statistically representative sample, but instead selected households to reflect the diversity of livelihood strategies, income levels (within the low-income range), and household structures that exist across Kenya. The final sample reflects those intentions with 31% of households in urban areas and 69% in rural areas, quite similar to

the distribution of 32% and 68% respectively from the 2009 national census.

In terms of poverty, 72% of the Financial Diaries households get by on less

than the equivalent of USD 2 per day (KSh119 per day). The remainder are still

low-income, with 95% falling below a USD5 per day threshold.

It provides a new and deep view of how Kenyans get by on low-incomes and offers new insights into how they use and think about their money. These insights can be quite useful to institutions serving the poor, offering up new perspectives on how the financial barriers to saving, borrowing, health care, education, and investing might be overcome.

Here some of the most important or un-expected results:

Where can you fit the unexpected?

Incomes are pieced together from multiple sources. The median

household in our study had 10 separate income sources registered throughout

the Diaries year.

Households face high levels of volatility in both income and

consumption spending. Like poor people around the world, our Kenyan

respondents face a combination of low-incomes and much uncertainty

and volatility in their spending needs and ability to generate income. For

the median household, income fluctuated ± 55% from month to month

and consumption fluctuated ± 43%.

Resources received from the social network – are a very important source of income, particularly for rural households and women. Resources received were not just large in number, but also as a share of total income; this was particularly so in rural areas, where resources received accounted for 25% of income in the median

rural household, versus just 6% in urban households. Eighty-five per cent of women in the study received income from this source. These contributions help cover basic needs but also enable families to stretch and cover unexpected expenses. As a result, they have a smoothing effect in rural areas, helping to reduce some of the volatility in income that these households otherwise experience.

Respondents emphasise savings more than borrowing. At the end of the study, the median household held the equivalent of 129% of their monthly income in financial assets, versus the equivalent of about 53% of their monthly income in liabilities.

This saving is active and not immediately avaitable in liquid form.

Our respondents appear averse to leaving money idle. Instead, they want to see their savings working – providing some immediate benefit – whether that is in buying consumption goods or physical assets, producing immediate returns, enabling them to borrow, or enabling a friend or relative to make an investment today.

The full report is available online. And please: READ IT. This tiny blog does not even capture a quarter of the interesting lessons the financial diaries offer.

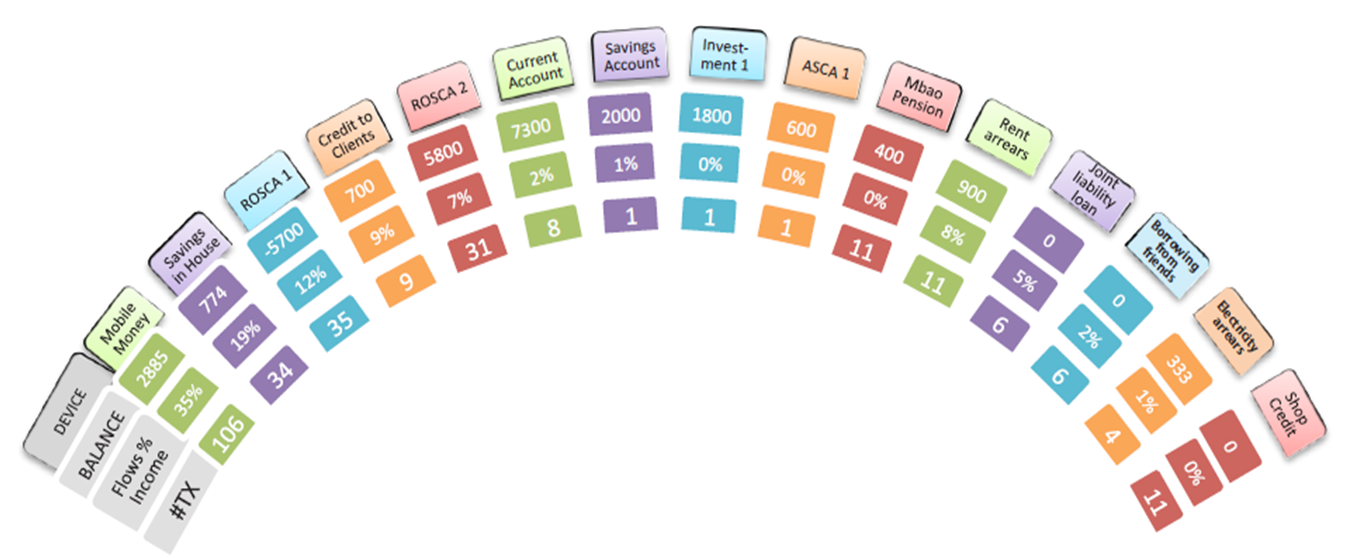

16 different financial

devices to help Patrick meet different kinds of needs.