Is this a question or a statement? There are quite some unanswered questions about microfinance institutions developing alternative delivery channels, such as agent or ATM networks or other mobile financial services. Do microfinance institutions have sufficient institutional capacity, sufficient resources to implement these channels well? Will such implementation deviate too much management attention from their actual core competency: lending to the poor?

Is this a question or a statement? There are quite some unanswered questions about microfinance institutions developing alternative delivery channels, such as agent or ATM networks or other mobile financial services. Do microfinance institutions have sufficient institutional capacity, sufficient resources to implement these channels well? Will such implementation deviate too much management attention from their actual core competency: lending to the poor?

OR: are alternative delivery channels actually the only option for microfinance institutions to compete with traditional banking institutions, since such a low-cost channels might be better adapted to the needs of the rural poor, might be cheaper to set up and manage and therefore present a viable channel options in rural areas with low transaction volumes?

However, there are quite some people working on finding answers and one is the Partnership for Financial Inclusion which I already mentioned in another blog earlier this year. I personally have been working on agent banking during my time at CGAP. However, our knowledge about the profitability of such agent networks was still limited when we wrote our publication “Banking Through Networks of Retail Agents.” The presentation which I found now is based on the work with 7 MFIs in the context of the IFC-MCF Partnership and includes some very interesting insights:

- Agent networks represent the most viable strategy to reach scale where branches are not viable, if:

- marketing and promotion activities allow the MFI to acquire large numbers of people;

- the MFI can dedicate significant resources to encourage customers to use the channel;

- the MFI is able to transform its organisation, systems, products, to create a customer experience which supports adoption.

- Most MFIs start with cash transaction at the agent. Over time, additional services (air time top up, bill payments, P2P transfers) are added.

- Transaction revenues will not cover the cost of the channel. An MFI expecting to grow from 100k to 400k customers can count on a net loss based on the channel reaching as much as USD2million per year. A moderate profitable MFI will burn around USD 5 million in accumulated losses before reaching profitability in year 4.

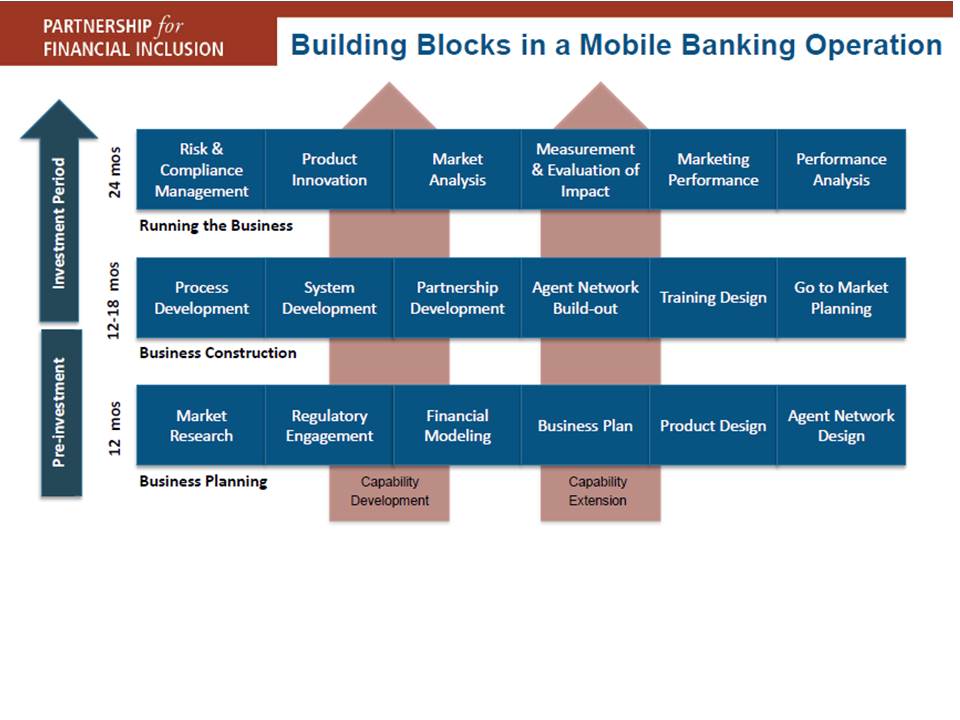

This does not sound easy, especially not for an MFI with less resources, less staff capacity, less..less..less.. The capacities needed during the different stages of implementation are also provided in the presentation:

The next blog will present some of the strategic options on how to set up a mobile financial services channel. Wait for it!