I have been always very much focused on the more usual products in microfinance, i.e., deposits, loans, transfers, etc. However, microinsurance is becoming more and more important. Due to my current mini-project with the MicroInsuranceNetwork, I actually had to learn very quickly what this product is about, how it is being delivered to low income clients, what the current challenges are, and what the regional differences are in terms of coverage.

MICROINSURANCE – A DEFINITION: Evidently there are many definitions and they have been subject of much debate and discussion.The definition of microinsurance is continually evolving:

- The protection of low-income people against specific perils in return for regular premium payments proportionate to the likelihood and cost of the risk involved (Preliminary Donor Guidelines, 2003).

- A risk transfer device characterised by low premiums and low coverage limits, and designed for low-income people not served by typical social insurance schemes (Micro Insurance Academy, India, 2007).

- Insurance that is accessed by the low-income population, provided by a variety of different entities, but run in accordance with generally accepted insurance practices. Importantly this means that the risk insured under a microinsurance policy is managed based on insurance principles and funded by premiums (International Association of Insurance Supervisors, 2007).

- A mechanism to protect poor people against risk (accident, illness, death in the family, natural disasters, etc.) in exchange for insurance premium payments tailored to their needs, income and level of risk (ILO’s Microinsurance Innovation Facility, 2008).

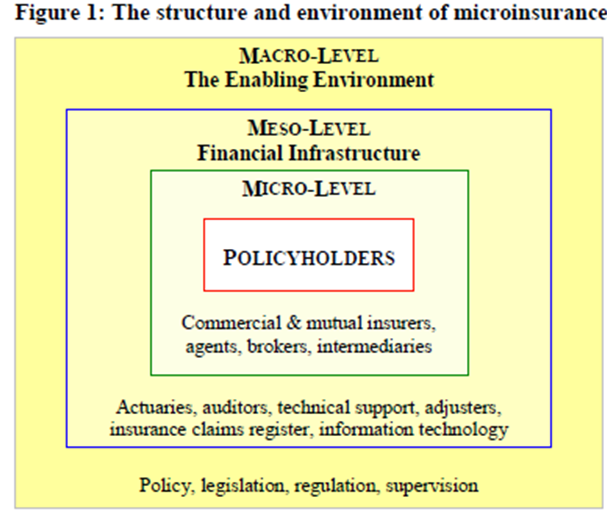

STRUCTURE AND ENVIRONMENT OF MICROINSURANCE

(the following is is primarily taken from “The Landscape of Microinsurance in the World´s 100 poorest countries which provides a wealth of information on microinsurance, but its content might make this blog more of a book than a short and crisp trigger)

Like microfinance, microinsurance also requires the coordinated actions of institutions on the three levels of the financial system: the micro, the meso, and the macro level.  Evidently the micro-level is made up of the policy holders (i.e., the end client) and the microinsurers. The insurer can be a single institution that carries the risk, markets and distributes the product, and administers the policy.

Evidently the micro-level is made up of the policy holders (i.e., the end client) and the microinsurers. The insurer can be a single institution that carries the risk, markets and distributes the product, and administers the policy.

The meso-level provides the financial infrastructure needed to facilitate the functioning of micro-level activities, e.g., actuaries are needed to assist the insurer to understand the risk in relation to a product and in setting premiums appropriate to the risk they have accepted. Meso-level organisation also include training facilities for microinsurance managers and staff and the availability of adequate software.

On the macro-level, we are looking for an enabling policy environment and conducive regulation to set the rules, to supervise insurers. In addition, governments need to regulate meso-level actors like actuaries or claim adjusters, plus they should play an active role in consumer protection.

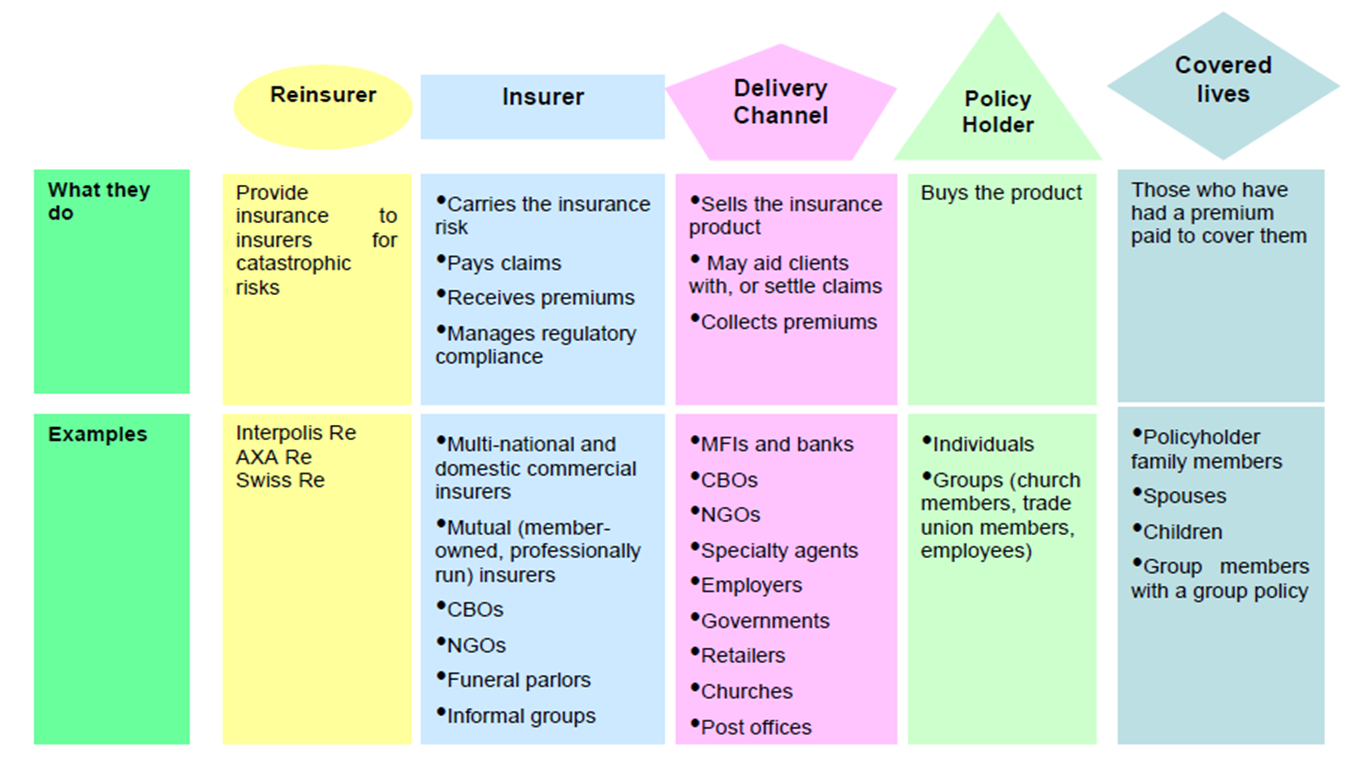

THE MICROINSURANCE SUPPLY CHAIN

The Reinsurer: Insurers hold reserves allowing them to pay for normal claims but would be insufficient for claims if all policy holders claimed simultaneously. Reinsurers are special type of insurers who “insure the insurers” against excessive losses. These players normally do not play a large role in microinsurance.

The Reinsurer: Insurers hold reserves allowing them to pay for normal claims but would be insufficient for claims if all policy holders claimed simultaneously. Reinsurers are special type of insurers who “insure the insurers” against excessive losses. These players normally do not play a large role in microinsurance.

The insurers: The most important task of the insurer is to carry risk and pay the claims. Since they carry the risk insurers have a final say in setting the price and ensuring that the product can control some of the risk. There are regulated and unregulated insurers.

The Delivery Channel: this is the organisation or individual selling and servicing the insurance policy, the most common being the insurance agent, however they are not very common in microinsurance. The reason being that insurance agents are typically paid via the commission they earn on the policy they are selling. However, in microinsurance with its tiny premiums, this is often seen as not worth it. Evidently with regard to the delivery channel, one should also keep in mind technology and how mobile phones or other devices could support the sale of microinsurance in the future (this looks like a future blog to me :))

Policy Holders: The policy holder pays the premium and makes the claims. A policy holder can be an individual or a group. In microinsurance individual policy holders are less common than groups, the reason being that it is much cheaper to sell small value policies to all group members than to sell to individuals (e.g., trade unions often buy “in bulk” for their members).

Covered lives/property. Covered lives are the people whose lives are insured. An individual can take out a life insurance policy on all members in his/her household. This is different from beneficiaries who are simply named as recipient of the claim settlement in case of of loss.

OUTREACH OF MICROINSURANCE

An article published on the Microinsurance Network website presents very well the challenges around measuring uptake of microinsurance around the world.

The often cited figures are 500 million, a number first published in Protecting the Poor, A microinsurance compendium (vol.II) in 2012, and 260.34 million, as cumulated from the first round of landscape studies in Latin America (2011), Africa (2012) and Asia (2013).

The compendium uses back-of-the-envelope calculations to estimate 500 million, based on data from 2006 and 2009, as well as various region specific 2011 data. These are used to extrapolate sector growth in different regions, and thus estimate total coverage ranges for each region. Over the past three years, the landscape studies have collected data on 1,264 microinsurance products, from 838 providers, in 102 countries throughout the developing world. They offer a more concrete, but significantly lower statistic with 260.34 million total coverage.

This blog is the center piece and links to blogs to different regional studies:

Microinsurance in Africa: 2012

Microinsurance in Asia /Oceania: 2012

which one should probably read once you understood some of the basics around microinsurance.