THE 2015 BROOKINGS

FINANCIAL AND DIGITAL

INCLUSION PROJECT

REPORT

We all know that an increasing number of developing countries are committing towards clear goals with regards to financial inclusion. For example, in May 2015, 54 institutions across 61 countries have signed the Maya Declaration on Financial Inclusion proving their recognition of the importance of financial inclusion, affirming the power of peer-to-peer knowledge sharing, expanding the Alliance of Financial Inclusion networks, developing a financial inclusion policy, implementing sound regulatory frameworks, recognizing the importance of customer protection, and using data to track progress towards financial inclusion.

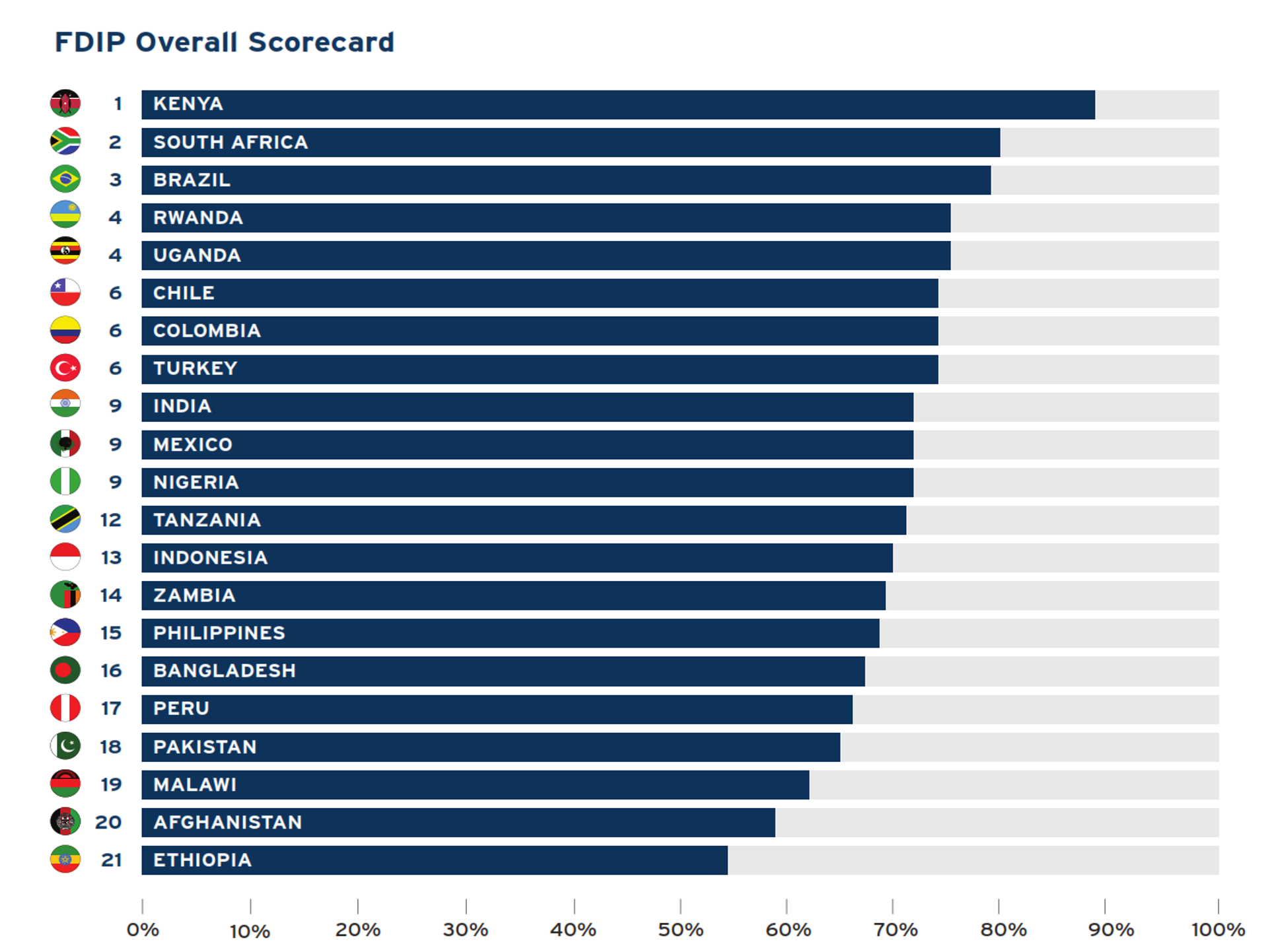

The Center for Technology Innovation at Brookings has launched the 2015 Brookings Financial and Digital Inclusion Project (FDIP) Report and Scorecard, which evaluates access to and usage of affordable financial services across 21 countries which have recently made commitments to financial inclusion and reflect political, economic, and geographic diversity.

Brookings experts analyzed the financial inclusion landscape in 21 geographically, economically and politically diverse countries, including Afghanistan, Bangladesh, Brazil, Chile, Colombia, Ethiopia, India, Indonesia, Kenya, Malawi, Mexico, Nigeria, Pakistan, Peru, the Philippines, Rwanda, South Africa, Tanzania, Turkey, Uganda, and Zambia, said the institute in a press release on Aug. 25. In the study financial inclusion was defined as “access to and use of formal financial services providing opportunities for facilitating individual prosperity and economic development.” Countries received scores and rankings based on 33 indicators spanning four dimensions: Country commitment, mobile capacity, regulatory environment and adoption.

And they even made a movie to accompany the report.

The FDIP report sought to answer the following questions:

- Do country commitments make a difference in progress toward financial inclusion?;

- To what extent do mobile and other digital technologies advance financial inclusion?; and

- What legal, policy, and regulatory approaches promote financial inclusion?

Key findings of the report:

Key findings of the report:

- Countries are making good progress towards financial inclusion, especially when mobile money is available.There are multiple pathways to financial inclusion which can be identified: e.g., in Kenya it is mainly mobile money service driving access to finance, where as in Latinamerica, access is driven much more via banks with less importance on mobile money. There is no one size fits all approach, but rather multiple pathways;

- Non-bank financial service providers play in increasing role in financial inclusion

- Among the first 10 countries in the report’s overall ranking, you find 5 from Africa (Kenya, South Africa, Rwanda, Uganda, and Nigeria). Tanzania is only coming in 12th. Four are from Latin America (Brazil, Colombia, Mexico, Chile). But there is none from Asia!?

- Country commitment towards financial inclusion is fundamental and does matter. Most countries that have committed are moving forward.

- The movement toward digital financial services will accelerate financial inclusion. Digital provides a huge opportunity and advantages in terms of efficiency

- Geography generally matters less than policy, legal, and regulatory changes, although some regional trends in terms of financial services provision are evident.

- Central banks, ministries of finance, ministries of communications, banks, nonbank financial providers, and mobile network operators play major roles in achieving greater financial inclusion. Coordination is an extremely important factor which plays an important part in advancing financial inclusion, e.g., governments and private sector

- Full financial inclusion cannot be achieved without addressing the financial inclusion gender gap. There is still a persistent gender gap under which women are significantly more excluded than men. The countries need to work on closing this gap.

- Cultural differences are highly important to point out. Different countries have different infrastructure which has to be taken into account when measuring progress towards financial inclusion.

I participated in a Brookings-organized webinar on August 26 2015 and here the list of panelists and their main messages:

Shawn Donnan, Financial Times, moderator. He is new to the sector and is just getting into the jist of microfinance, access to finance, financial inclusion, digital financial services, etc.

Loretta Michaels, US Dpt of the Treasury. Mrs Michaels was responding to the question what the interest of the treasury was with regards to financial inclusion. She mentioned that it was a high priority for the Treasury primarily due to its economic impact and the impact on stability of financial markets. The lack of financial exclusion provides problems in many markets, besides economic ones, financial inclusion is a priority when considering saveguarding the global financial system from ALM and CFT. Consumer protection was also mentioned as another big issue for the Treasury.

Leora Klapper, World Bank: Mrs Klapper gave a brief description of the current landscape from the World Bank’s FINDEX report. Especially with regards to the gender gap, digital payments provide control, privacy, lower crime, womens’ economic development, time which is normally spent waiting in line, credit histories based on payment histories, etc.etc.etc. BUT there are also still challenges, e.g., considering identification (e.g., Bangladesh: women do not have any ID document), the handling of PIN numbers is still a problem for many countries, and trusting a mobile money scheme si also a barrier towards adoption.

Jerry Grossman, GSMA: Mr Grossman focused more on the MNO perspective. He started with a general observation that the 21 studied countries were highly diverse with regards to their income levels (e.g., middle to upper income down to very low income countries), but 3 of the top 5 countries (Kenya, Uganda, Rwanda) were very low income and ranged higher than many of the higher income countries. In the past and still today, Subsaharan Africa sees more development of mobile money deployments since it has developed strongly its regulatory environment and capacity. More and more people are adopting mobile financial services, but it is not adoption which is important, but active usage (90 days as measured by the GSMA). Mobile money is not anymore a Kenyan story, but with the right regulatory environment it can develop anywhere. Today, in Africa it is mainly mobile operators driving the financial inclusion agenda. However, without taking side between banks and mobile network operators (MNOs), there is a great potential for digital financial services and the pie is huge to be shared between banks and MNOs. MNOs have the infrastructure, the “rails”, but need the products which are currently offered by the banks or insurance companies.

Karen Miller, Women’s World Banking: Mrs Miller was answering the question: why this gender gap? According to her, it does not need much to get women to open accounts, but providers will have to better understand what women want, understand their needs, develop a product that corresponds to their needs, e.g., savings is a critical component for this. Women do not have the time to stand in line in branches, i.e., digital financial services serve these needs, plus they serve women’s demand for security, and confidentiality is another big issue. I really liked her image that digital financial services nad savings products went together like peanut butter and jelly.

Tidhar Wald, Better then Cash Alliance: Mr Wald described the strong movement from cash to digital payments which is undertaken by many governments and where many governments realize collateral effects when developing a digital financial transactions ecosystem (e.g., ghostpayments are detected). He mentioned India where the government launched a new financial inclusion scheme, and in no time they had opened 175 million new accounts in one year. Roughly 50% of these accounts have a zero balance. The government tries to actively reduce dormant accounts by channeling as many G2P payments via the network.

It was an interesting discussion with a good group of people (all very US based and minded). However, I was missing the new stuff. I am not convinced that the FDIP report really provides that much new knowledge than the global FINDEX report. There is a lot of money spend in producing these new studies and often we are just looking at another side of the coin but the coin is still the same.

For those of you with more comments on the FDIP report, please send them to FDIPcomments@brookings.edu.

In addition to the report, the website also provides 21 country examples, and a list of frequently asked questions which are quite interesting.