Zambia is one of these countries for me about which I do not know anything. This might be a good thing for an African country since many of them get into the headlines for not so positive things like currency devaluations, droughts, or sacked central bank governors. What was the last thing I heard about Zambia? I have no idea…..

Zambia is one of these countries for me about which I do not know anything. This might be a good thing for an African country since many of them get into the headlines for not so positive things like currency devaluations, droughts, or sacked central bank governors. What was the last thing I heard about Zambia? I have no idea…..

Well, I thought, let´s have a look at this country from an access to finance perspective.

Here a few headlines:

PEOPLE: 14.6 m people (estimated in July 2014…. We are just in April 2014, but ok….) of 20 different ethnic groups with 19 different languages (…. Uihhhh that does not sound like fun), 66% of the population is younger than 24.

POVERTY: around 68% live below the poverty line and the GDP per capita reaches USD1,800. 85% of the population lives of agriculture. The GIni Index reaches 50.8%.

OTHER INDICATORS: around 38% of the population lives in urban areas. Mobile penetration is up to 78% (whow!), but financial services penetration is only 23%.

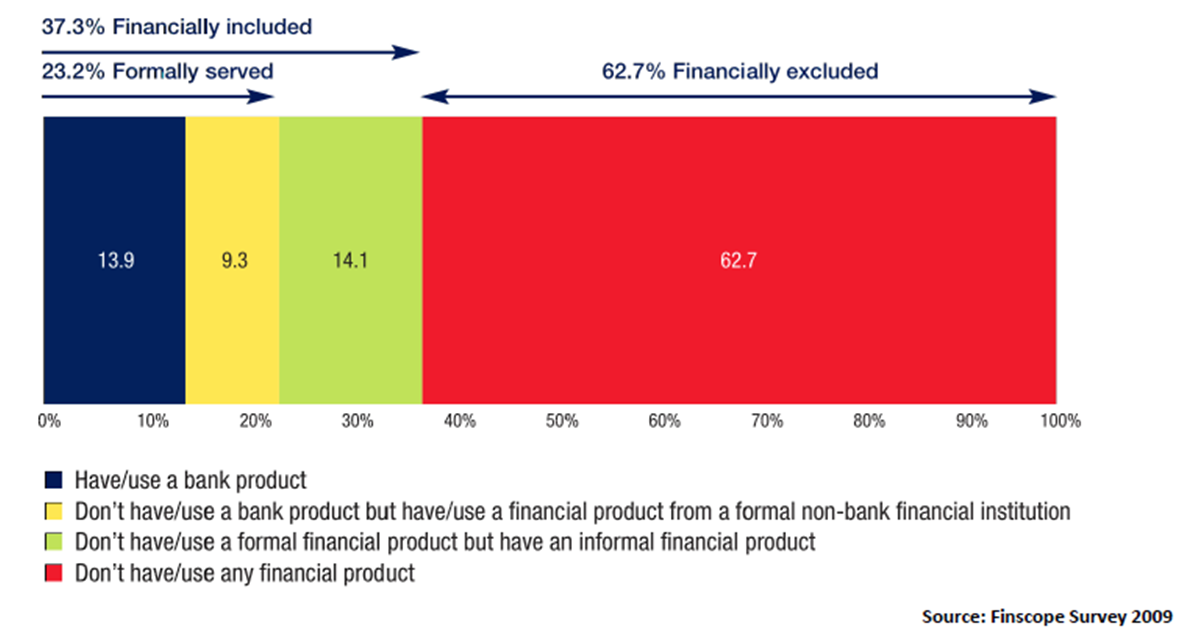

FINANCIAL ACCESS: The 2009 Finscope Survey conveyed the following lessons: 66% of rural female adults and 59% of rural male adults do not have access to financial services. Of those with access in rural areas, many use informal channels. 59% of adults do not save at all. (i.e., 6 out of 10 Zambians living day to day without any risk mitigation strategy). 67% of MSMEs (micro, small and medium enterprises are tiny, owner-operated businesses with no employees.

FINANCIAL INFRASTRUCTURE: There are around 286 bank branches for around 19 banks (Nine-teen!!! Of which no real identifiable microfinance bank. On the Mix, you find a list of 10 microfinance providers including known names such as FINCA, PRIDE, etc. with in total 75,677 borrowers 🙁 and an outstanding loan portfolio of USD28.2m 🙁

There seems to be a Microfinance Association of Zambia (AMIZ) which is constantly underresouced and and unable to play its part in coordination and advocacy of the microfinance sector.

CONCLUSION: Whow! This sounds like a very poor country with no existing access to finance for its population. At the same time this might be an opportunity for some of our greenfield networks. The high mobile phone penetration might enable providers to use cheaper delivery channels and not follow the general brick-and-mortar holy grail

This is untapped territory!

Sources: DFID Zambia. Access to Finance Programme. Business Case, DFID May 2012, The World Fact Book, The Mix, Bankable Frontier Associates. Mapping the retail payments landscape in Zambia. Commissioned by Finmark Trust.