No time to read it? Let me do it and write out the main messages for you:

No time to read it? Let me do it and write out the main messages for you:

Most of us know the data: 2.5bn people unbanked and relying on informal financial services which are unsafe, inconvenient, and expensive. However, 1bn people have access to a mobile phone which could provide access to a wide range of services. Since 2009, the Mobile Money for the Unbanked (MMU) programme helps mobile money services to develop services for the underserved and thereby pushing financial inclusion.

Building on the Mobile Money for the Unbanked programme, the GSMA launched the Mobile Money Interoperability Programme including partners like Axiata, Bharti Airtel, Etisalat, Millicom, MTN, Ooredoo, Orange, Telenor, Turk Telekom, Vodafone and Zain.

This initiative is accelerating interoperability of mobile money services by identifying and sharing best practices, guidelines and processes and providing regulatory support in a number of leading markets. In 2014, operators in Pakistan, Sri Lanka and Tanzania interconnected their mobile money services, allowing their customers to send money across networks within those countries.

Here the highlights from the 2014 State of the Industry Report:

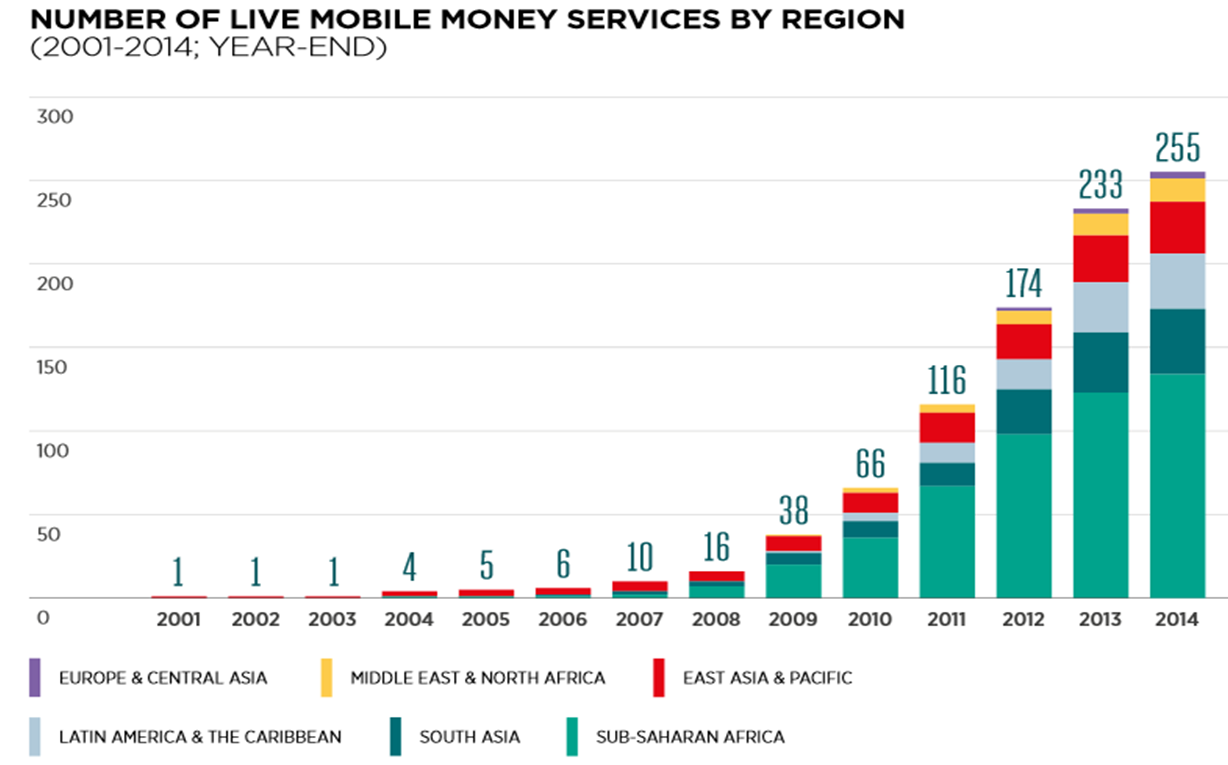

- 255 mobile money services are now live across 89 countries (compared with 233 live services across 83 markets at the end of 2013). In over 61% of developing markets, mobile financial services (MFS) are firmly established in the financial sectors of the majority of the developing world. Sub-Saharan Africa accounts for the majority of live services globally (53%), half of all launches in 2014 occurred outside the region, with Latin America & the Caribbean, East Asia & Pacific and South Asia all seeing 3 new launches, respectively. Today, Europe & Central Asia is the only region with more planned than live mobile money services. With mobile money maturing, the number of launches is falling every year. Twenty-two new services launched in 2014 (including

Dominican Republic, Myanmar, Panama, Romania, Sudan and Timor-Leste), compared with 59 launches in 2013 and 58 launches in 2012.

- The number of registered mobile money accounts globally grew to reach 299 million in 2014. These accounts only represent 8% of mobile connections in the markets where mobile money services are available. In 2014, seven new markets joined the ranks of countries with more mobile money accounts than bank accounts. 16 markets now hold this status, indicating that mobile money remains a key enabler of financial inclusion.

-

The industry is getting smarter about what it takes to prompt mobile money adoption: There are 103 million active mobile money accounts as of December 2014 and an increasing number of services are reaching scale. Twenty-one services now have more than one million active accounts.

-

Providers are now becoming increasingly adventurous by expanding into adjacent markets for mobile financial services, leveraging their strengths in mobile money to provide mobile insurance, mobile savings and mobile credit to customers who previously never had access to formal financial services. The interviews revealed four key challenges that mobile money providers may need to consider when developing a rural strategy:

-

Overcoming logistics and delivery challenges: A lack of infrastructure in rural areas creates logistical challenges for agent and cash management. Leveraging local partnerships, flexible agent financing, and smarter transactional data analysis are enabling providers to address these challenges.

-

Identifying and communicating a compelling value proposition: Understanding the nuances of how rural consumers earn, save, and spend their money can help providers develop a relevant value proposition for rural users, which may well be different to that of their urban users;

-

Creating a user-friendly service and accessible interface: As rural customers tend to have lower financial and technical literacy levels, the service will require a user-friendly interface to enable access. While technologies such as IVR can be useful for reaching illiterate users, greater investment in customer education and increased “touch-points” are also proving successful as a means of on-boarding customers in rural areas;

-

Finding solutions to the lack of formal identification documents: The absence of compulsory population registration and identification is a common barrier to wide-scale adoption of mobile financial services, but it is evenmore prevalent in rural areas. In most markets, regulation plays an important role; solutions such as tiered KYC and adjusting acceptable KYC documentation can help providers facilitate customer adoption in rural areas.

-

-

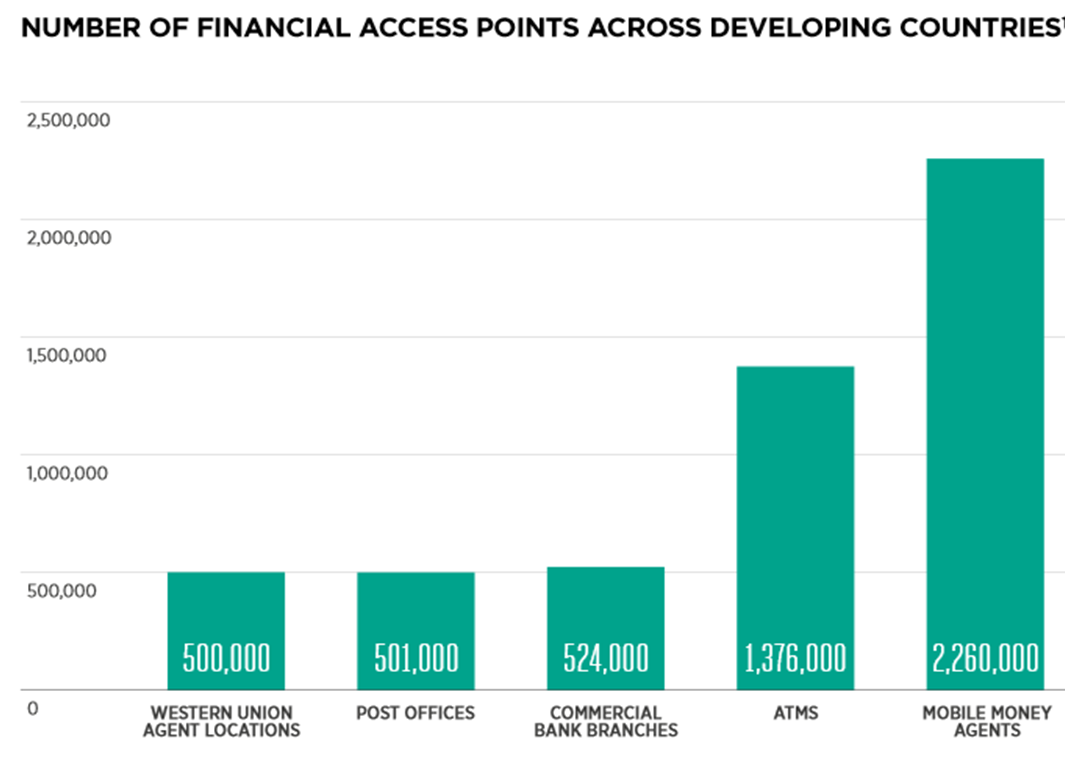

The number of mobile money agent outlets grew by 45.8% in 2014, reaching a total of 2.3 million globally in December. This is particularly impressive if we consider the size of traditional financial institutions’ and remittance services’ networks. In three-quarters of the 89 markets where mobile money is available today, agent outlets outnumber bank branches. In 25 of those markets, there are more than ten timesas many mobile money outlets as bank branches. The total number of active mobile money agent outlets that facilitated at least one transaction during the month grew by 44.2%, rising from 946,000 in December 2013 to 1.4 million in December 2014.

NUMBER OF FINANCIAL ACCESS POINTS ACROSS DEVELOPING COUNTRIES

-

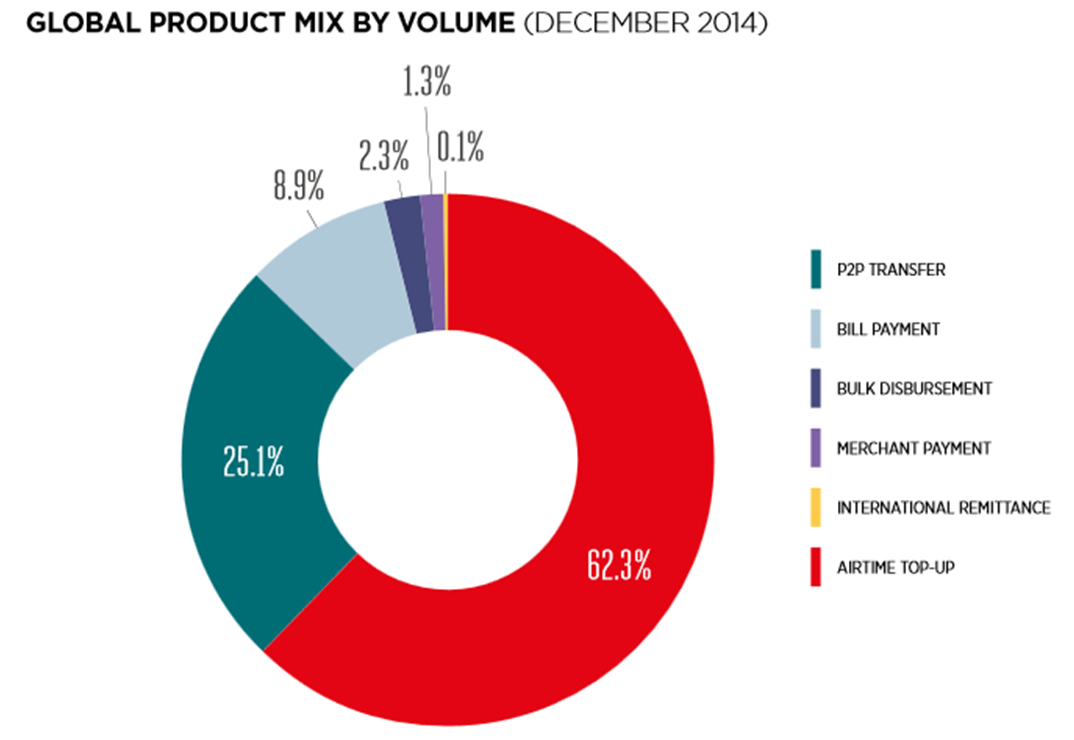

P2P transfers and airtime top-ups still dominate the global product mix in terms of volume and value, however, the fastest growth in 2014 occurred in bulk disbursements, bill and merchant payments – reflecting an expanding ecosystem of institutional and business users of mobile money;

GLOBAL PRODUCT MIX BY VOLUME

-

2014 saw a steep increase in the number of international remittances via mobile money, primarily driven the new model of using mobile money as both the sending and receiving channel. Mobile money helps to reduce the costs of international remittances for users: survey respondents reported that the median cost of sending USD 100 via mobile money is USD 4.0, less than half the average cost to send money globally via traditional money transfer channels.

-

Where mobile money is yet to launch suggests there are two prevalentreasons for this: Challenges to

-

building a solid business case due to addressable market size and territory size: Today, 54 developing countries do not have a live mobile money service. 70% of these countries have a population of less than 10 million. A small addressable market size makes it harder to build a business case for investment in mobile money, since it is more difficult for a mobile money service provider to achieve scale,lower costs and reach profitability. In addition, many of these markets are small territories, where it can be harder to build a P2P use case.

- regulatory hurdles: Just 13 of the 54 developing markets where mobile money services are not yet available have a population of over 10 million. 14 launches are planned in these 13 markets, indicating a high level of interest from mobile money providers. However, in most of these countries, the regulatory approach appears to be slowing down the launch of services.

-

- Main regulatory reasons slowing down providers to launch or to scale (according to survey respondents):

- Transaction/balance limits too low and/or onerous customer identification requirements: AML/CFT including KYC requirements may simplify customer due diligence (CDD), however, misapplying these recommendations with onerous identification requirements will slow the uptake of mobile money.

- No interest earned on pooled funds or no permission to use interest earned:

Passing on the interest earned on pooled funds to mobile money customers is very effective for increasing transactionality and would not change the nature of the trust accounts or the role of the non-bank providers (which are not permitted to intermediate the funds).

-

Restrictions of international remittance business: While a number of countries allow in-bound international remittances to be received on a mobile money account, many countries have restrictive laws on outgoing remittances, limiting the ability for mobile money providers to connect their accounts across borders

Whow, there is a lot of interesting information in this report. However, I think with the messages above, I squeezed out the most important ones.

Want to leave me a comment?

[contact-form]